The fintech arena

Fintech is a term describing companies combining technology and finance. It often relates to small startups which bring to the market innovative technical solutions. Over the last years, those fintechs have been developing a blooming offer of financial services that are not available from banks. Banks are now facing a competition coming mostly from those technology driven providers.

The services fintechs provide are, for the time being, focusing on simple and standardized products which are not knowledge intensive and that are not generating the biggest margins. They also try to focus on products that are not regulated too much or take advantage of grey areas in the regulation, not requesting banking licenses. This phenomenon has been growing steadily over the last years in particular in the US and in the UK.

The services fintechs provide are, for the time being, focusing on simple and standardized products which are not knowledge intensive and that are not generating the biggest margins. They also try to focus on products that are not regulated too much or take advantage of grey areas in the regulation, not requesting banking licenses. This phenomenon has been growing steadily over the last years in particular in the US and in the UK.

|

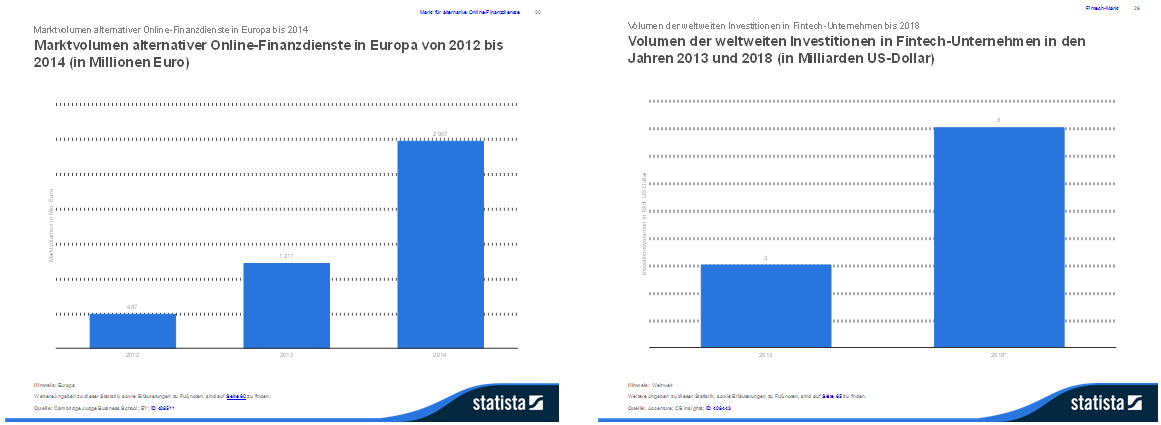

Volumes going through fintech companies grew from 487M€ in 2012 to almost 3B€ in 2014. Regarding investments, 3B€ have been invested in fintechs in 2014 and the forecast for 2015 is to triple, reaching more than 12B€. The number of VC involved and the amount invested are increasing quickly: 520M€ in 2010 up to 2,8B€ in 2014 invested by 55 VCs in 2010 and 216 VCs in 2014 (Source Statisca). Those VCs are predominantly coming from the US and Asia is lagging a bit behind: in 2014, 1.8B€ from the US, 569M€ from Europe and 330M€ from Asia (Source Statisca).

Fintechs have been initially addressing the easiest segment: payments and they are gradually expanding to all segments in particular banking and corporate finance which has been developing significantly:

This growth is surfing on the banks’ lack of innovation in particular regarding digital products. New comers are bringing up to date technology to the market in particular in the real time area where banks are far away. Banks’ technology is sometimes more than 40 years old and mostly based on mainframe technology working in batches. Hardly anything is real time, most actions and events are taken into account the day after. Customers are now used to internet and the real time capacity it offers. Even if banks have invested a lot in online banking it still suffers from the batch mode impacting the user experience. |

New entrants are not only startups but also big established internet companies like Apple with the payment service Apple Pay, Google with an equivalent service named Google Wallet, the telcos like Orange which has a banking license and will enter the market in 2016. Those companies have a huge technological capacity and they already own customers. Furthermore, there are, at least for some of them, managing the hardware customers are using: they can manage an end to end user experience from the device to the service. What happened in the media industry is summarized by this quote from Jeff Bezos, Amazon’s CEO: “We are not building devices for technology freaks. We are building devices for people who like to consume and use media. We don't want to make money on the devices, we sell them at cost price and hope that we then make money from the Amazon offering that is linked to the devices. That is films, books, newspapers, games and apps.”. Those technology players are in a good position to offer a great user experience.

Another example is Facebook which just introduced micro payments within members. With 1.4 Billion users including shops, restaurants, Facebook could withdraw a lot of transactions from the regular banking system.

Another strong point of those new entrants is their capacity to analyze data, including personal data, using up to date technologies (Big data). This gives to fintech companies the ability to offer more targeted services to customers or profile their customers better and quicker.

Those companies tend to integrate better in the whole chain. For example payment services provided by fintechs are without much effort integrable in any web or mobile site. This is a differentiating factor compared to banks which have most often much less efficient technologies. For the company owning the web or mobile app, it is beneficial to have a seamless integration at an affordable cost.

But as seen earlier, payments is not the only market fintechs are looking at. The main fintech categories so far are (source Statisca): Payments, Banking and corporate finance, Capital markets, Data analysis, Personal finance management

Inside those categories there are a lot of different types of activities. Banking and corporate finance includes peer to peer lending (consumer or/and business), crowdfunding (reward based or Equity based), community shares (lending small sum to small businesses), invoice trading just to name a few.

Data analysis is an interesting emerging category were fintechs collect financial data on individuals, markets or corporate in order analyze this data in a more efficient way using up to date technologies to analyze huge amount of data. They often use machine learning capacities to bring differentiating capabilities to the market. Examples of this are credit risk scoring or insurance data analytics.

Fintechs in the Capital markets area are more software vendors than true service providers. The knowledge is more important in that area and capital needs are huge.

Personal finance management has been developing a lot including areas like Wealth management and tools to visualize and aggregate all personal banking information in an easy and comfortable way.

As mentioned earlier, fintechs are attacking banks in different point of their value chain. Together they have a large coverage of the products than can be automated. Their capacity to move on more knowledge based products remains to be seen. But their current scope can be already harmful for banks